Hybrid mismatches under scrutiny: Analysing Belgium's latest circular

On 22 October 2024, the Belgian Tax Authorities ("BTA") published a circular letter on hybrid mismatches, which provides comprehensive guidance on the application of Belgium's anti-hybrid mismatch rules (Dutch/French). As a reminder, the latter rules, which have been in force since 1 January 2019, are derived from the EU Directives ATAD 1 and ATAD 2 and are designed to prevent tax avoidance through hybrid mismatch arrangements.

Although the circular letter seems to predict increased scrutiny by the BTA as regards cross-border arrangements, it also provides greater legal certainty for taxpayers, given the many clarifications and examples on the application of these complex rules.

The most relevant aspects of this circular letter can be summarised as follows:

- Explanation of definitions

The circular letter contains a clarification of the definitions that are used in the relevant Belgian legal provisions, of which the most important are:

- Hybrid arrangement: this is an arrangement that results in deductible expenses for a Belgian company or a Belgian establishment and for a foreign company or one of its establishments, or for one of those stakeholders but without corresponding income being included in the taxable income of the recipient. Hence, this definition targets both mechanisms of "double deduction" (deduction of the same expense by two taxpayers) and mechanisms of "deduction without inclusion" (deduction of an expense without taxation of the corresponding income). It should be noted that only stakeholders qualifying as associated enterprises, which are part of the same company or are operating in the framework of a structured arrangement, are envisaged by this definition.

- Hybrid entity: this concerns an entity that is treated differently for tax purposes in different jurisdictions, i.e. an entity that is treated as a taxable entity under the laws of one jurisdiction and whose income and expenses are treated as the income and expenses of one or more other persons under the laws of another jurisdiction.

- Hybrid transfer: this includes the transfer of a financial instrument where the underlying return of the transferred instrument is treated for tax purposes as if it is simultaneously received by more than one of the parties involved in the arrangement.

- Clarification of targeted hybrid mismatches and corresponding tax adjustments

In a subsequent section, the circular letter deals with several cases of targeted hybrid mismatches and the related tax adjustments, each time accompanied by a specific example. In this regard, the following adjustments are envisaged:

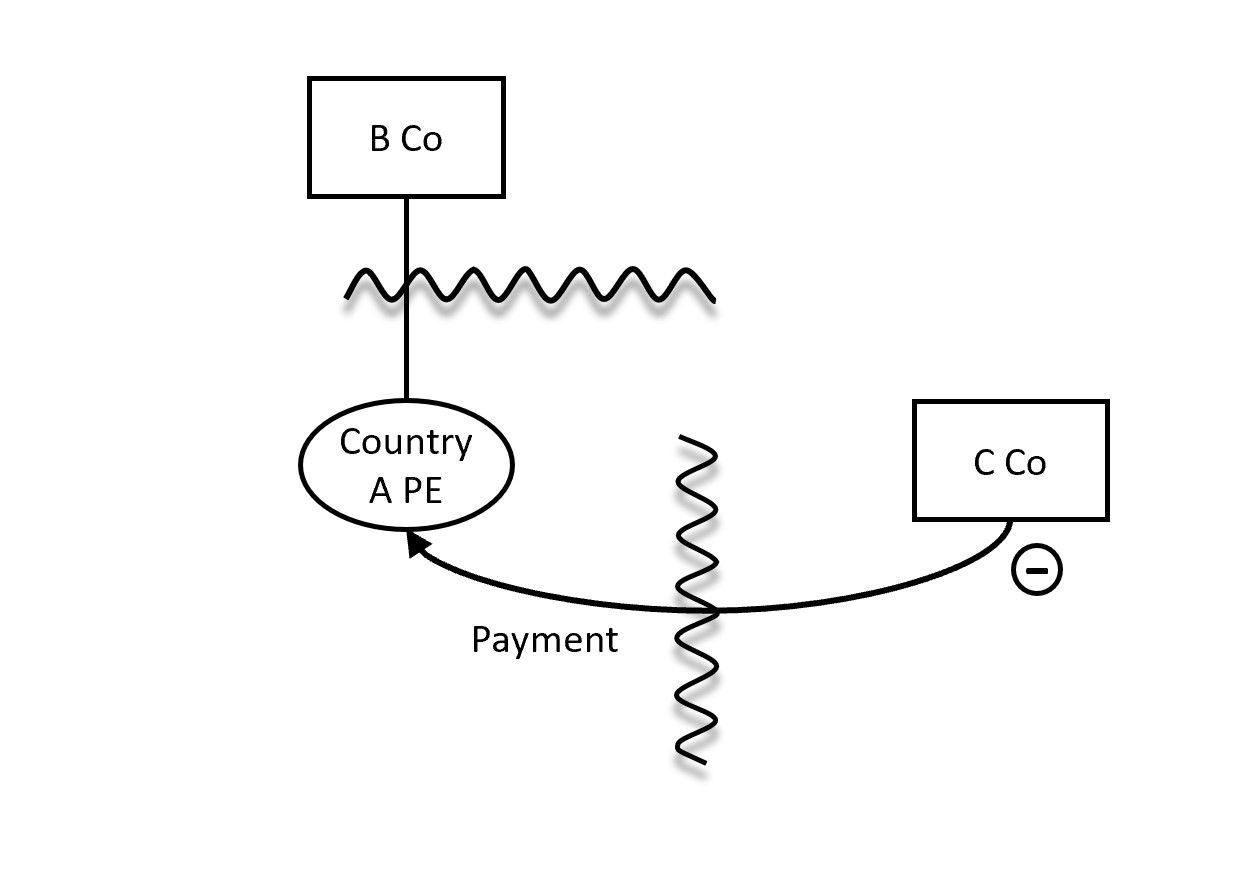

- Adjustments resulting in an increase of the taxable basis: an example where this adjustment is applied concerns a Belgian company that has a permanent establishment ("PE") in another EU country. If a foreign entity makes a tax-deductible payment to that PE, and the payment is not taxed in the country where the PE is located (because it is not recognized as such), the amount will be included in the taxable basis of the Belgian company. This adjustment ensures that the income is taxed in Belgium if it is not taxed in the other jurisdiction.

- Adjustments resulting in a non-deductible cost:

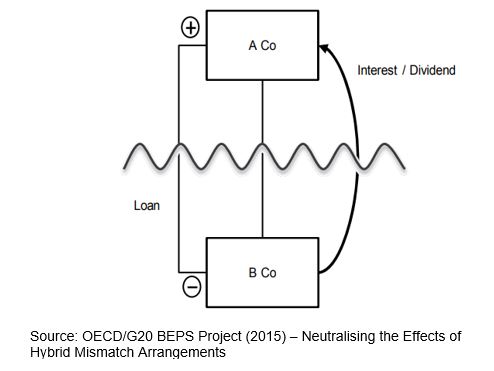

- This adjustment can be applied in case there is a deductible payment in Belgium without the inclusion of a taxable income abroad. For example, a foreign company owns all shares of a Belgian company and provides a loan to the latter. Under Belgian law, the loan is treated as a debt instrument and the payments are considered as deductible interest, while, under the laws of the foreign country, the loan is treated as an equity investment and the payments are considered as dividends. Consequently, the deduction of the interest payments is denied in Belgium to the extent that they are not included as income in the taxable basis of the recipient.

- It is important to note that also "imported hybrid arrangements" are envisaged. These are hybrid mismatches that occur between foreign stakeholders, resulting in double deduction or deduction without inclusion in their respective jurisdictions, with a Belgian stakeholder making payments to one of these foreign participants. In such case, the deduction of such payment is rejected in Belgium, unless the other jurisdictions neutralize the effects of the hybrid mismatch themselves.

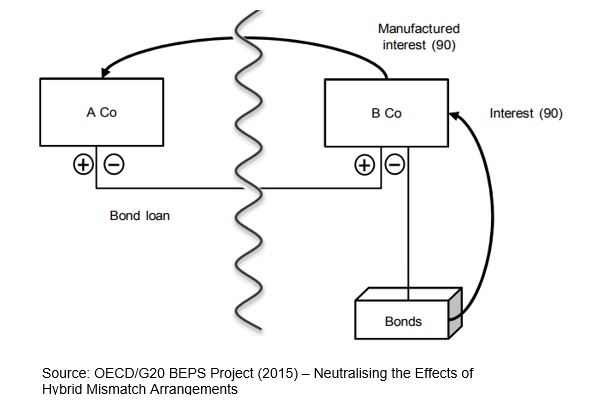

- Limitation of the foreign tax credit ("FTC"): this applies in case of hybrid transfers aimed at obtaining tax credits for the same withholding tax in several jurisdictions. For example, a foreign company lends bonds to a Belgian company and a compensation payment is made by the latter to the first mentioned for interest, net of a 10% withholding tax. In case the interest amounts to EUR 100, the Belgian company will make a compensation payment of EUR 90. In such case, the FTC in the hands of the Belgian company is limited to the tax on the net income (i.e. EUR 10) from the hybrid transfer.

As the publication of this circular letter probably indicates that the BTA will closely monitor cross-border transactions, it is likely that the number of tax audits on this topic will increase as well. Therefore, Belgian companies must carefully assess their cross-border investments and comply with these regulations to avoid adverse tax outcomes, with special attention to imported hybrid arrangements.

In case of questions, please do not hesitate to reach out to your regular contact within the Fieldfisher Belgium tax team.