Leveraged Equity Distributions: Interest Tax Deductibility Confirmed

In two recent judgments (10 December 2024 and 18 February 2025), the Ghent Court of Appeal ruled that interest paid on loans financing capital reductions or dividend distributions (i.e. leveraged equity distributions) are tax deductible.

These judgments contrast with the rather negative case law to date in this area (e.g. Ghent, 9 January 2018, n° 2016/AR/1618; Ghent, 26 September 2023, n°2022/AR/513; Antwerp, 8 May 2018, n°2016/AR/2108; Antwerp, 28 September 2021, n°2020/AR/454). The pivotal issue in these cases typically revolves around the demonstration that the interest expenses are incurred to acquire or maintain taxable income at the level of the distributing company.

Context

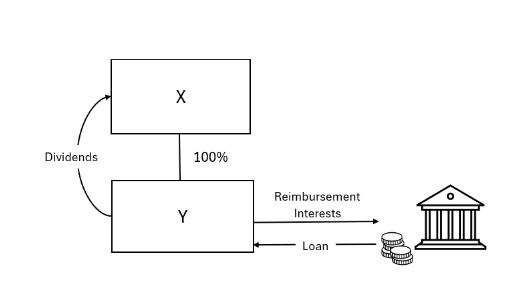

Operations where a company takes on debt to finance leveraged equity distributions has been a hot topic for some years in Belgium.

During the last decade, the tax authorities have increasingly challenged leveraged distributions based on a narrower interpretation of the deductibility conditions of Article 49 of the Income Tax Code of 1992. This led to a surge of litigation over the past decade, where tax authorities argued that such loans primarily benefited shareholders and impoverished the distributing company and hence that the related interest expenses were not incurred to acquire or maintain taxable income (the "finality condition" of the general tax deductibility conditions) at the level of the distributing entity. As a result, the tax authorities did not consider these interest expenses to be tax deductible.

This administrative position has been upheld by the Supreme Court ("Nyrstar judgment" of 19 March 2020 and "Duvel Moortgat judgment" of 31 March 2023), based on the lack of evidence to demonstrate that the finality condition was met. Although these judgments never confirmed this, in practice they led to a near-automatic administrative rejection of the tax deductibility of interest expenses relating to leveraged distributions structures.

Change of approach?

Recently, the Ghent Court of Appeal followed the above established principles but was apparently dealing with more substantiated cases. The Court rightly emphasized that the finality condition can be met in leveraged equity distribution structures to the extent that it is grounded on sufficient supporting evidence:

- Case of 10 December 2024: to demonstrate that the leveraged distributions were meeting the finality condition, the taxpayer relied on its financial statements to show that its main assets consisted of illiquid assets (e.g. shareholdings in other companies), which would not have allowed a distribution in cash without the need to realize them. Hence, the Court ruled that the interest is tax deductible given that the loan was necessary to prevent the loss of these assets while they were income-generative for the taxpayer.

- Case of 18 February 2025: the taxpayer's only substantial asset was a long-term receivable from another company within the same group, generating annual interest at 7%. The taxpayer argued that it could not proceed with the decided capital reduction without liquidating or transferring this asset. Consequently, a loan with an annual interest rate of 6.5% (resulting in a cost lower than the income generated by the receivable) was concluded. Based on key documents provided by the taxpayer, the Court ruled that the finality condition was met as the company did not have sufficient assets to carry out the distribution without realizing its assets. As this receivable was the taxpayer's only income-generating asset, preserving it seemed essential to ensure the company's (future) taxable income generation.

Key takeaway

The commented judgments of the Ghent Court of Appeal confirm that interest expenses relating to leveraged distributions can be tax deductible. To be tax deductible, taxpayers must be able to demonstrate among other things that the finality condition is met. Hence, these judgments confirm again the necessity for taxpayers to dispose of sufficient evidence.

***

In case of questions, please do not hesitate to reach out to your regular contact within the Fieldfisher Belgium tax team.